Higher investment growth is found in equity markets. I am retiring at the end of December, although I will only be turning 65 on 21 April 2026. I have the option to take all of my provident funds, but I prefer to pay no costs and go the fixed deposit route, either with Aluma or Nedbank. What other options are available?

Dear reader,

It is possible for you to withdraw the full provident fund value and invest it in a fixed deposit. However, to assist you in making an informed decision, I’ve provided some relevant information.

Potential benefits

- By withdrawing your full provident fund value, the capital becomes discretionary in nature. This means that the capital is fully available to you at any time. If you transfer your provident fund value (or a portion of it) into a life annuity or living annuity, the capital in the annuity won’t be fully accessible as these products only pay out an income amount.

- As the capital will be discretionary in nature once it has been withdrawn from the Provident Fund, any income drawn from this capital will not be taxed as it is not, technically speaking, an income, but simply a withdrawal of your own capital. However, the growth in capital, that is the interest earned on this capital, will be taxable. That being said, individuals who are 65 years of age and older qualify for an interest exemption of R34 500. This means that interest earned up to this amount is tax-free. Interest earned above this amount will be taxed as per the marginal tax rates.

- Investing the capital into a fixed deposit is a safe and secure way to achieve a fixed return. There is no market volatility and returns are predictable. There is also no need for ongoing investment management and therefore there are no investment management fees.

Potential negatives

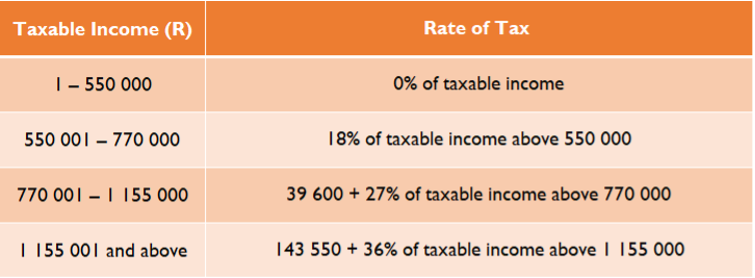

- Depending on the value of your provident fund, there may be tax implications as per the retirement fund tax tables. Up to R550 000 is tax-free, provided no previous retirement fund withdrawals were made. Withdrawing an amount in excess of your tax-free portion will attract tax. I’ve included the retirement fund tax tables for your interest.

- A fixed deposit often requires you to ‘lock’ your money in for a certain period. This may hinder your ability to structure an appropriate income plan and may also mean that funds may not be immediately accessible to you in the event of an emergency.

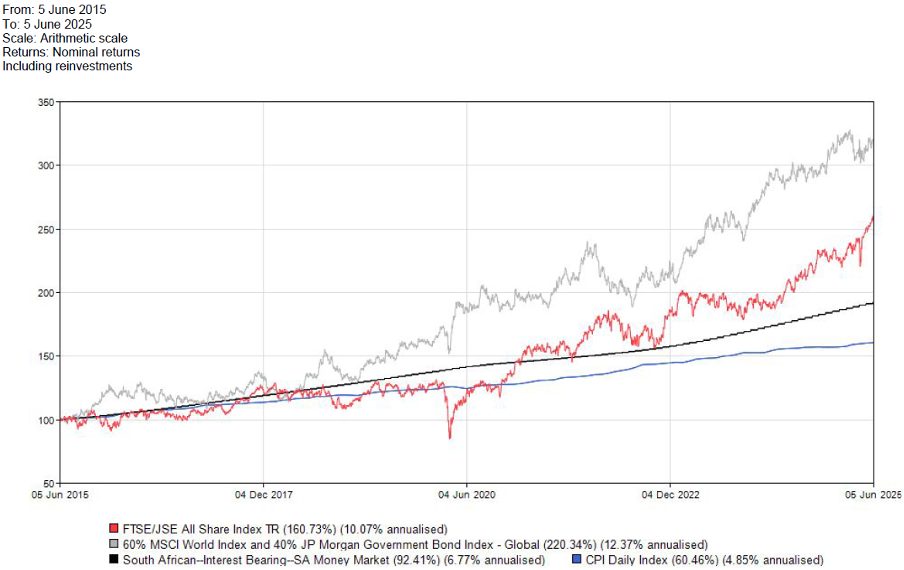

- We can’t say for certain, but interest rates are possibly heading lower. This means that the fixed rate from a fixed deposit may not be as good as the returns that could be earned from investing in the markets — even after the additional fees. I have included a graph below showing historical performance over the last 10 years. Ultimately, even after accounting for fees, history tells us that higher investment growth is found in equity markets, both locally and globally.

- With a living annuity, you can nominate beneficiaries, and on death, the nominated beneficiaries can immediately inherit the assets. With a fixed deposit, the funds will have to go into your estate. An estate can easily take two years or longer to wind up and your beneficiaries will have to wait until the estate is wound up before they can access the funds.

In conclusion, I would highly recommend seeking professional advice from a certified financial planner who is registered with the Financial Planning Institute of Southern Africa. This will ensure that you receive experienced and sound advice. The advice can assist you in a number of ways. For example, it is possible to determine the tax-free portion available to you or the tax payable on the full withdrawal of your provident fund. It can also assist you in achieving your specific objectives in the most cost- and tax-efficient manner.

All the best for your retirement.

Read: First meeting with a financial advisor? Here’s what to ask